YOUR TAX YEAR-END CHECKLIST

We are fast approaching the end of the 2025/26 tax year, meaning now is the ideal time to review your financial position and ensure you are making full use of available tax allowances and reliefs. Acting before the deadline will help you manage your tax liabilities more efficiently, increase your savings, and reduce the amount of tax you pay.

This blog outlines key actions you may wish to consider and act on before it’s too late.

Pensions

Making pension contributions remains one of the most effective ways to save for retirement. It also brings down the amount of personal tax owed. Pension contributions automatically benefit from a tax relief with basic rate taxpayers receiving a 20% tax relief and higher rate tax payers receiving 40%. This increases further to 45% for additional rate taxpayers earning over £125,140.

Increasing your workplace pension contributions can automatically lower your income tax, as pensions are taxed at source. For self-assessments and personal pensions, you will automatically benefit from 20% relief; however, you will need to reclaim additional tax relief (if applicable) when filing. For more information on this, please refer to GOV.UK

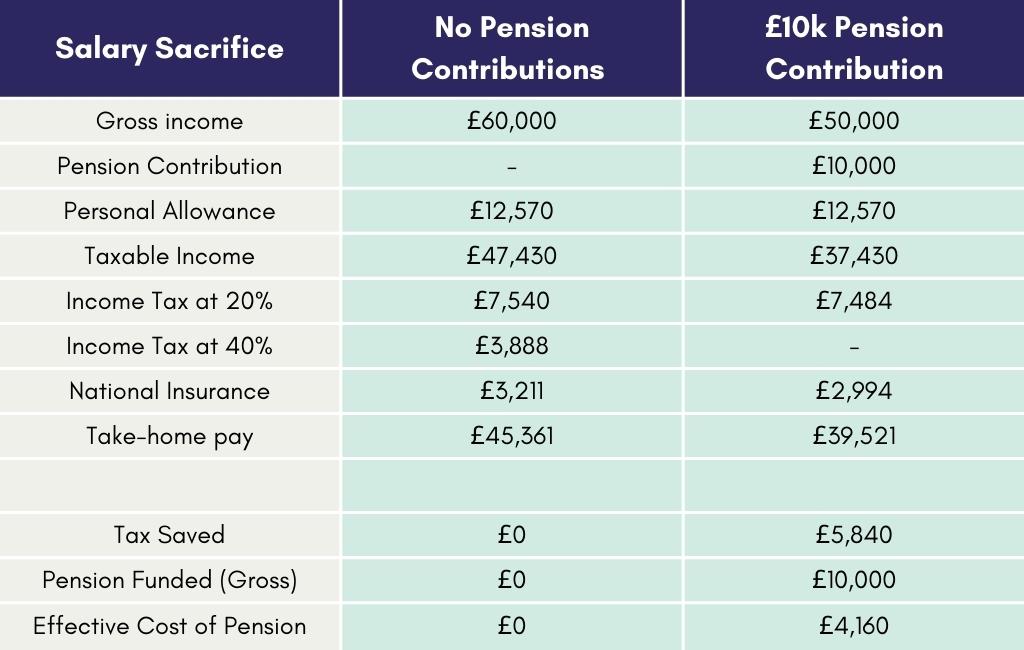

Here is an example of how significant this can be in reducing tax liability through a salary sacrifice pension:

In this example, £10,000 goes straight into the pension before tax and National Insurance. As a result, the contribution costs only £4,160 in take-home pay by saving £5,840 in tax and NI overall.

Note: You do not benefit from reduced National Insurance on any pension contribution that is not done via salary sacrifice, such as private pensions, Net pay arrangements (NPA) or Relief at source (RAS), however you will still benefit from a reduction of income tax owed as illustrated in the above example.

What is the current pension allowance?

The annual pension allowance for the current financial year (2025/26) is £60,000 or 100% of your relevant UK earnings, whichever is lower. There is no longer a lifetime allowance, meaning you can continue to accrue pensions. Previously, this was set at £1,073,100. While you can continue to make pension contributions, pension funds are not accessible until the minimum pension age (currently 55, rising to 57 in 2028). You can withdraw up to 25% of the accrued pension, which is capped at the previous lifetime allowance, or up to £268,275, with the remainder being taxable at the marginal rate of income tax.

National Insurance Savings via Salary Sacrifice?

From April 2029, the National Insurance advantages of pension salary sacrifice are expected to change. At the moment, salary sacrifice can be a tax-efficient way to contribute to a pension, but under the proposed rules, only the first £2,000 of contributions each year will remain free from both employer and employee National Insurance. Any salary sacrificed above that level would attract employer National Insurance at 15%, and employee National Insurance at between 2% and 8%. The good news is that income tax relief on pension contributions isn’t changing, so pensions will remain a very tax-efficient way to save for the future.

It’s also worth noting that this cap only applies to pension salary sacrifice arrangements. Other schemes such as cycle-to-work or electric vehicle salary sacrifice plans, are not affected, and employer pension contributions made outside of salary sacrifice will still remain free from employer National Insurance. In reality, this change is likely to affect higher earners or people making larger pension contributions through salary sacrifice. For most people, nothing needs to change right now. However, if you have a significant salary sacrifice arrangement in place, it’s sensible to keep an eye on developments and review things closer to April 2029 once HMRC releases more detailed guidance.

Maximise 2025/26 ISA allowance

For the 2025/26 tax year, you can invest up to £20,000 across one or more ISAs. This allowance can be split across different ISA types, including:

- Cash ISA: tax-free savings

- Stocks & Shares ISA: tax-free investing

- Lifetime ISA (LISA): first-time buyers or retirement planning (up to £4,000 of the total allowance

You will incur a lifetime ISA government withdrawal charge (currently 25%) if you transfer the funds to a different ISA or withdraw the funds before age 60, and you may therefore get back less than you paid into a lifetime ISA. By saving in a lifetime ISA instead of enrolling in, or contributing to, an auto-enrolment pension scheme, occupational pension scheme, or personal pension scheme:

(i) you may lose the benefit of contributions from your employer (if any) to that scheme; and

(ii) your current and future entitlement to means tested benefits (if any) may be affected.

For ISA Investors, do not pay any personal tax on income or gains, but ISAs may pay unrecoverable tax on income from stocks and shares received by the ISA managers. Tax treatment varies according to individual circumstances and is subject to change.

Looking slightly further ahead, a notable change is expected from 6 April 2027, specifically affecting Cash ISAs. For those under the age of 65, the maximum amount that can be paid into a Cash ISA each year will be reduced to £12,000. Crucially, any growth, interest, or income generated within an ISA is completely free from income tax and capital gains tax. Unlike pensions, ISA allowances do not roll over. If you don’t use your allowance by 5 April 2026, it is lost permanently. That means a missed opportunity for tax-free growth. Even modest, regular contributions can compound significantly over time when sheltered from tax.

If you have available cash or investments sitting outside an ISA, now is the time to consider whether moving them into a tax-efficient wrapper makes sense, as once the tax year ends, the opportunity is gone. Stocks & Shares ISAs are typically more suitable for longer-term goals because they give access to markets that may deliver higher returns over time, but remember, investments can fall as well as rise in value.

Junior ISAs

Sometimes overlooked, Junior ISAs are another way of reducing tax liability while building a financial head start for your children. This is a tax-free savings or investment account for children under 18, with an annual allowance of £9,000. This money belongs to the child and becomes accessible when they turn 18.

Capital Gains Tax (CGT)

As part of your year-end planning, it’s important to review any assets sold during the year and check whether you have used your full Capital Gains Tax (CGT) annual exemption, which currently stands at £3,000 per individual. This means the first £3,000 of profit (gain) from selling or disposing of an asset is tax-free, with the amount reduced to £1500 for the majority of trusts. If you still have unused allowance available, it may be worth considering selling assets before the end of the tax year to make use of it. For couples, transferring assets between spouses or civil partners can also be an effective way to utilise both CGT exemptions and reduce the overall tax payable.

Tax on Bonuses

Bonuses are taxable and should therefore be treated in the same way as any other income. It may come as a surprise to you how much tax is deducted from a bonus. This is usually because payroll systems assume that the higher pay for that period will continue for the remainder of the year, temporarily increasing the tax deducted. In most cases, this evens out over the tax year, but it can still create short term cash flow shock.

To minimise the tax impact on a company bonus, you may wish to use a salary sacrifice scheme to pay some or all of the bonus directly into your pension. Provided you have not already maximised your annual pension allowance, any amount paid into your pension in this way will be tax free. You can also choose to split the bonus, with a percentage paid into your pension and the remainder paid to you as income. Keep in mind that any portion paid directly to you will be taxable and could potentially push you into a higher tax bracket. It is worth checking the tax implications in advance so you are fully aware of any liabilities.

Other strategies to reduce tax include deferring the bonus to a lower earning tax year or investing in tax-efficient schemes such as Enterprise Investment Schemes (EIS), or using it for charitable donations. The options available to you will vary depending on your employment circumstances and the schemes your employer has in place.

Key Dates for UK Tax Year End

- Tax Year End: April 5th 2026

- Start of Next Tax Year: April 6th 2027

For the 2025/2026 Tax Year (Ending April 5, 2026)

- Self Assessment Online Filing Deadline: January 31, 2027

- Self Assessment Paper Filing Deadline: October 31, 2026

- Paying Tax Owed (for 2024/25): January 31, 2027

Act Now before it is too late

With the tax year-end fast approaching, any unused allowances will be lost if no action is taken. It’s a classic case of “use it or lose it.” When matters become more complex, particularly where higher-risk investments or business tax reliefs are involved, it’s important to seek professional financial support. I work closely with clients to help them maximise these opportunities in a way that aligns with their goals. If you would like to explore your options further before the deadline, please get in touch.

Disclaimers:

Approver Quilter Financial Services Limited March 2026.

The value of investments and the income they produce can fall as well as rise. You may get back less than you invested.

For ISA Investors do not pay any personal tax on income or gains, but ISAs may pay unrecoverable tax on income from stocks and shares received by the ISA managers.

Tax treatment varies according to individual circumstances and is subject to change.

Tax Planning is not regulated by the Financial Conduct Authority.

Sources:

GOV.UK, MoneyHelper

Ready to get started?

Get in touch today

If you would like to arrange a meeting with Sarah, please complete the attached form you can schedule in a 15 minute initial telephone call.