Review Your Spending: A Simple Way to Take Control of Your Money

Many people believe there is a specific gift tax in the UK, but this is not actually the case. You can gift money to family members without paying tax at the time the gift is made. However, gifts can still have Inheritance Tax (IHT) implications. If you give money away and then pass away within a certain time period, the gift may be considered part of your estate for tax purposes, depending on its value.

How much money can you gift tax free each year?

£3000 annual exemption

Each tax year, you can gift up to £3,000 without it being added to your estate for Inheritance Tax (IHT) purposes. This is known as the annual exemption, and it applies regardless of who you give the money to, not just family members. If you do not use the full allowance in a tax year, you can carry the unused amount forward to the following tax year. However, it can only be carried forward for one tax year.

For example, if you gifted a total of £1,000 in the 2024/25 tax year, you would have £2,000 of unused allowance remaining to gift. This means that in the 2025/26 tax year, you could gift up to £5,000 in total (£3,000 for the current year plus £2,000 carried forward) and remain within the annual exemption. For couples, the allowance applies to each individual. This means that if both partners carried forward their unused allowance, a couple could potentially gift up to £12,000 between them in a single tax year while remaining within the exemption.

Small Gifts Allowances

For small gifts of up to £250, you can give up to £250 per person per tax year to as many individuals as you like without affecting your Inheritance Tax position. This can be particularly useful for birthdays, Christmas gifts, or helping family members in small ways. It’s important to note that you cannot combine this allowance with the £3,000 annual exemption for the same person, so it’s worth keeping track of which exemption you are using. Many people overlook this, either because they are unaware of the tax rules or because they assume it won’t impact their estate, often believing the gifts will fall outside the relevant time period.

Wedding and Civil Partnership Gifts

For wedding or civil partnership gifts, HMRC provides specific exemptions. You can gift up to £5,000 if you are a parent, £2,500 if you are a grandparent, and £1,000 if you are anyone else, without the gift being considered for Inheritance Tax purposes. These allowances apply to each individual contributing and must be provided before or on the date of the ceremony for the exemption to apply.

What is the 7-year rule for gifts?

When you gift money or assets that exceed the available exemptions stated above, the gift is usually treated as a Potentially Exempt Transfer (PET). This means the gift will become exempt if the provider survives seven years after making it.

What happens if you die within 7 years of gifting?

If you die within seven years of making a significant gift, Inheritance Tax may apply. In many cases, the amount of tax payable can be reduced through taper relief, which gradually lowers the tax due the longer the person who made the gift survives after giving it. Typically, it is the gift recipient who is responsible for paying any tax due, although this can depend on how the deceased’s estate has been structured. Understanding these rules is important for both the gift giver and the recipient.

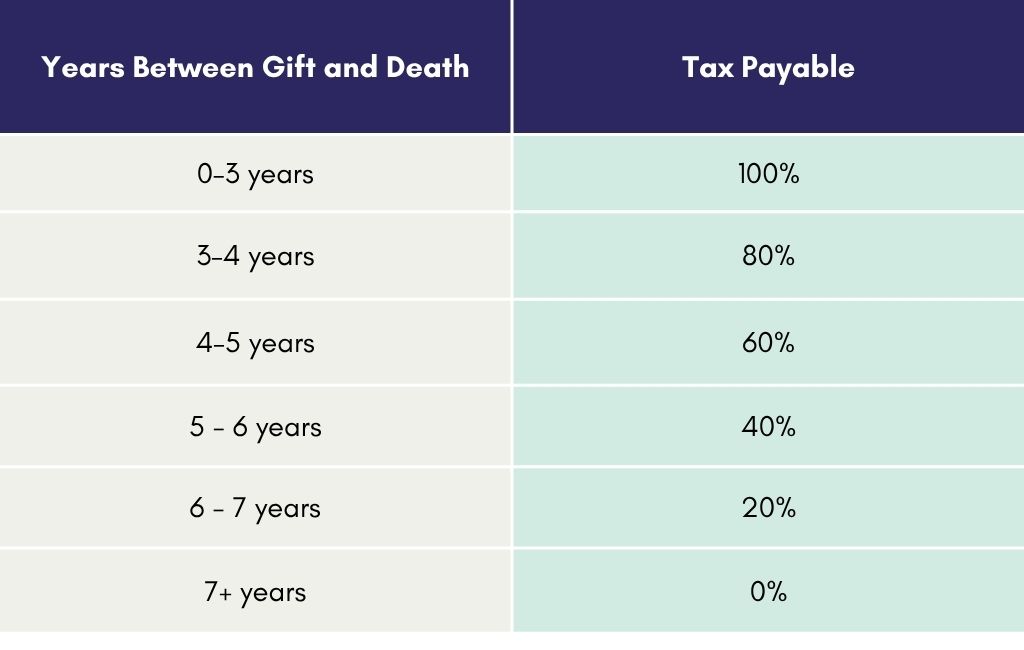

The table below shows how taper relief is typically applied when calculating the tax payable.

Based on the above, let’s assume that you gift a family member £10,000. As this amount exceeds the £3,000 annual exemption, it is treated as a Potentially Exempt Transfer (PET).

If you pass away within the first three years, the full amount (£10,000) will be considered when assessing the tax liability, with Inheritance Tax currently charged at 40%. If you were to pass away in year six, but before year seven, then 20% of the 40% tax would be payable due to taper relief.

This is sometimes misunderstood, with people thinking the tax they pay is based on their income tax rate. Gifts and inheritance are not taxed under income tax in the UK. Instead, they fall under UK Inheritance Tax, which is a completely separate tax system.

Can You Gift Regular Income Without Paying Tax?

This is a particularly useful rule known as gifts out of surplus income. If you have income that exceeds your normal living costs, you may be able to make regular gifts without them being subject to Inheritance Tax. The key condition is that the gifts must come from income rather than capital. This generally includes income received after tax from employment or a pension, the natural yield from investments such as interest or dividends, and rental income. The gifts must also be made regularly and must not impact your standard of living. Proper documentation is essential, as HMRC may require evidence showing that the gifts were made from genuine surplus income. There are no fixed intervals for making regular gifts; they could be monthly, quarterly, or annually.

Are there any limits on gifting to money to children?

There are no legal limits on how much money you can give your children. However, large gifts, as discussed earlier, may fall under certain Inheritance Tax rules if you die within seven years of making them. If the recipient is a minor (under 18), there are also practical considerations around how the money is managed. Many parents choose to set up Junior ISAs to help ensure the money is used effectively while still benefiting from tax advantages. There are, however, restrictions on how much money you can contribute to a Junior ISA each year. For more information about ISAs, including Junior ISAs, please refer to: What Is a Stocks & Shares ISA and How Can It Help Grow your Wealth?

Can I gift my house to my children?

It is possible to gift property to your children, however this can have complex tax implications, particularly if you continue living in the property after the gift has been made. In situations like this, the property may still be considered part of your estate for Inheritance Tax purposes under rules known as a “gift with reservation of benefit.” This means that even though ownership has been transferred, HMRC may still treat the property as belonging to you for tax purposes if you continue to benefit from it.

It is more common for people to pass property to their children as part of their estate after death, through the instructions set out in their will. However, this may still be subject to Inheritance Tax if the total value of the estate exceeds the applicable thresholds. Because property transfers can also trigger other considerations, such as Capital Gains Tax or Stamp Duty implications depending on the circumstances, it is often advisable to seek professional guidance before making a decision.

For more information relating to Inheritance Tax, please refer to go GOV.UK

How to Gift Money Safely and Tax-Efficiently

If you are planning on gifting money to family members, then it is sensible to plan this carefully. By keeping records of gifts, documenting them either electronically or as a paper copy, and storing them safely, it will make things far easier in the long run if you or your loved ones need to supply records in the future.

In certain circumstances, setting up a trust may be the most appropriate option for managing larger gifts or protecting assets. It is also important to ensure that gifting decisions relating to your estate are reflected in your will and overall estate plan, so everything aligns with your wishes as intended.

When Should You Speak to a Financial Planner?

In many cases gifting can be straightforward, however the tax implications can become more complex for larger estates, blended families, property transfers and business owners. A financial planner can help structure your gifts in a way that protects or reduces the liability of tax implications for the gift receiver.

A financial planner can help you structure gifts in a way that supports both your family and your long-term financial security. In some cases, strategies such as life insurance policies designed to cover potential inheritance tax liabilities can also form part of the planning process.

At Astute Financial Planning, I can help you make informed decisions around gifting to family members and how this fits within your wider financial and estate planning. Please contact me to arrange a free initial consultation.

Disclaimers:

Approver Quilter Financial Services Limited March 2026.

Tax treatment varies according to individual circumstances and is subject to change.

Advice on cash held on Deposit, Tax Planning and Inheritance Tax Planning are not regulated by the Financial Conduct Authority.

Sources: GOV.UK

Astute Financial Planning and Quilter Financial Planning are not responsible for the accuracy of the information contained within the linked sites.

Ready to get started?

Get in touch today

If you would like to arrange a meeting with Sarah, please complete the attached form you can schedule in a 15 minute initial telephone call.